0N_TECHSTORM Geopolitics Edition - Spring 2024

The Global Battle for Power, Resources, and Prosperity Intensifies ...

For my Spring 2024 Techstorm Forecast, I’m going all-in on the geopolitical perspective on technology. In recent years, we’ve seen a tremendous shift from globalization to sovereignty, isolationism, and “America First!”. Although this shift is a perfectly natural reaction to ongoing conflicts and supply chain hiccups after Covid, it’s a slippery slope down to a more closed and hostile world.

I can agree that the just-in-time global supply chain gospel sold to CEOs all over the world by large consultancies was taken a bit too far and became way too fragile. But the flip side to this is that we’ve created a large (and growing) middle class in Eastern Europe, China, and to a certain extent also India, Indonesia, and other countries. Close to a billion people have entered into this consumer class in the last couple of decades. I just wished they took the train to an ecolodge in rural Sweden instead of posing outside of a Louis Vuitton store in Stockholm…

In the wake of more isolationism and anti-globalism comes the geopolitical quest for more power, specifically technological power. The USA and China are the main contenders, with Europe desperately trying to catch up. It’s an uneven fight where the US has the benefit of a large home market, an active government and military on the client/partner side, as well as the backing of a mature venture capital industry. China, on its side, has more of the same and also the “luxury” of being a totalitarian state that doesn’t have to kiss up to its voters every four years. Instead, they can ignore public opinion, work long-term, and think decades instead of years when strategizing.

China’s challenge is that its growth is slowing, and its quest for near-term world leadership has come to a halt, increasing diplomacy and outreach. Europe also has a growth problem but faces a different set of difficulties. Member states try to agree on common priorities and budgets while fighting a growing threat from a second wave of Brexiteers within their borders. Conflicts in their vicinity and a need for increased military spending add to this.

All is not doom and gloom, though. From my perspective as a small cog in the pan-European innovation/technology/investment ecosystem, I can definitely see some light at the end of the tunnel. The European startup and venture capital ecosystem is growing and maturing at a steady pace. I see more and more examples of companies and entrepreneurs relocating to Europe or choosing the continent as the best place to start and run their businesses. Talent is cheaper here than in Silicon Valley, quality of life is good, and freedom of speech in a less polarized environment is increasingly important to people. Add to this world-class research institutions and some of the best industry incumbents there are.

That said, we can’t rest on our laurels, things need to improve. We need more capital for tech investments and the green transition. Incumbents need to digitize and AI-tize at a much faster rate to stay in the race. Universities and scientists need to improve their ability to spin out and commercialize research. Finally, we have to update our view on risk-taking and failure as natural parts of improvement and learning, not the other way around. Needless to say, this list of challenges is not exhaustive.

End of rant @#%€&?!!

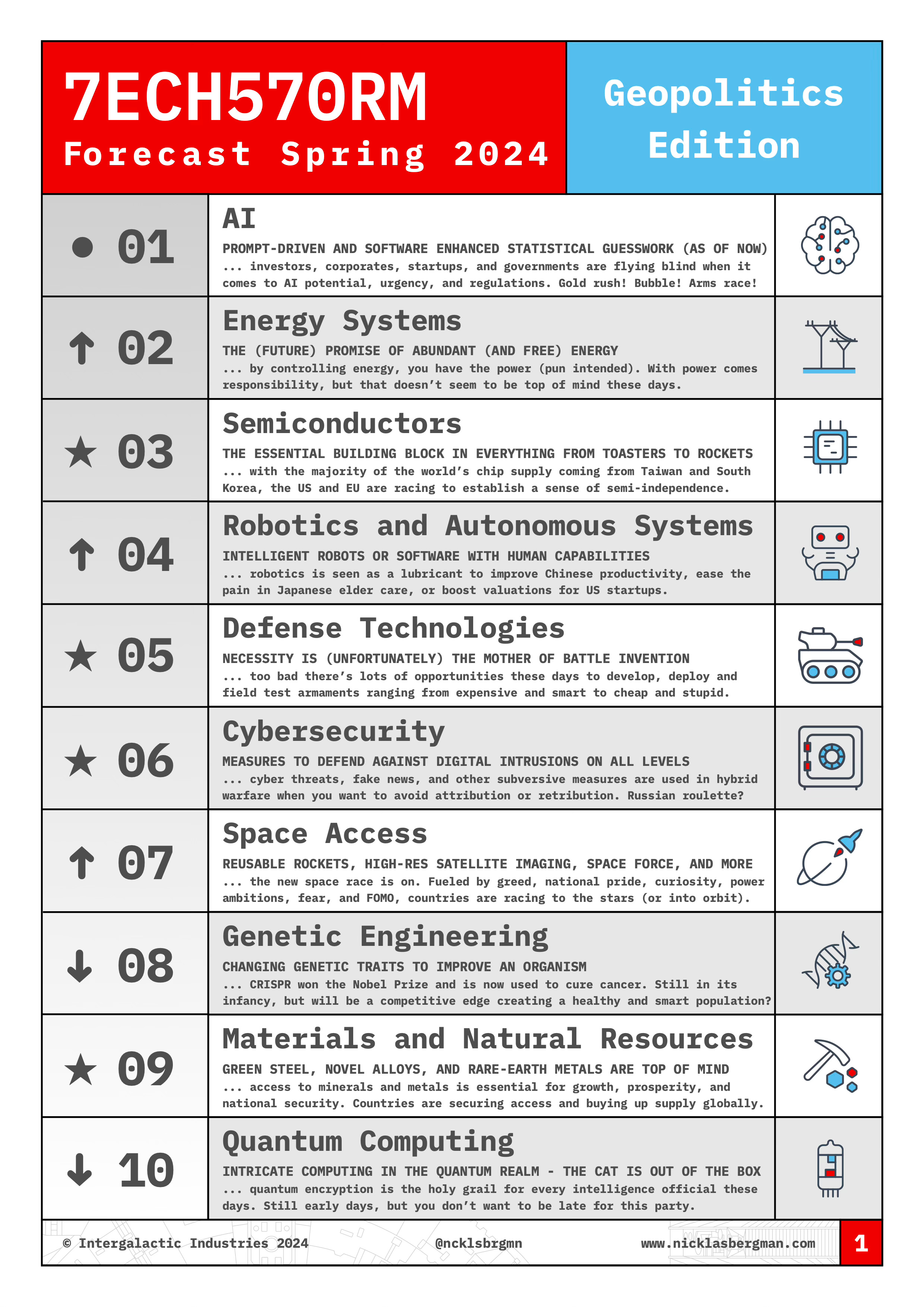

The Techstorm 2024 Spring Geopolitics Forecast:

AI is, of course, #1 on the list. Crazy amounts of money are being invested in everything with a heartbeat or .ai domain address. This is true for companies, investors, and institutions. Governments are launching AI initiatives and strategies, funding ethics research, and trying hard to regulate the use of AI. Companies seem to have an almost unanimous blind faith that generative AI is the holy grail of corporate development and VC investment. This is despite the fact that generative AI models are expensive to build, slow to run, and (as it seems) difficult to scale. Also, the jury’s still out there on whether the true value will accumulate at the level of the LLMs, the hardware suppliers (cloud included), or the applications.

For me, today’s hype around AI is a clear case of the classic Amara’s Law: “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.”

Another contender for the top of the list is Energy (production, supply, distribution, storage), where Europe saw last winter how fragile the system is. Now, betting on increasing the deployment of solar, wind, and nuclear power, European policymakers have to reverse their strategic decisions that rely on Russian gas and the termination of nuclear capacity.

With 21 reactors currently under construction, China is the new nuclear powerhouse (pun intended), and that’s more than all other countries combined. In comparison, the US has one reactor under construction. What’s also astonishing is that China is building reactors at a cost of 2 BUSD per gigawatt, compared to the US at 12 BUSD per gigawatt. Finally, some nuclear economies of scale! This also means that Chinese companies are exporting nuclear technology to the rest of the world, creating a dependency and lock-in through financing, construction, and maintenance for decades to come.

Access to cheap and reliable energy will be one of the main competitive advantages in the future!

It’s impossible to exclude semiconductors from this list. Too soon to forget the global shortage we had a couple of years ago. With most of the production of high-end semiconductors coming from Taiwan and South-Korea, we’re bound to expect continuing tensions and potential conflict as China increases its stronghold on Taiwan. TSMC, the #1 semiconductor manufacturer in the world, answers to this by moving production overseas to the US and Europe, of course with massive governmental support (billions of Euros and Dollars). Also, China is slowly but steadily catching up in this race, and the latest chip from the state-controlled foundry SMIC is only one generation behind their overseas competition. All in all, this could potentially mean that the South China Sea tensions could ease a bit.

What else?

Defense research and spending are reaching new heights, and NATO even has a VC fund. Everything from munition and autonomous robot defense systems to drones and lasers is top of mind these days. In this field, it’s not only a focus on innovation and advanced systems; also, production capacity, logistics, and training are getting well-deserved attention. This is clearly very true in the Russia - Ukraine conflict where, for example, Russian artillery use has gone from 50,000 shells per day in 2022 to 10,000 per day in 2024. Clearly an effect of limited supply and ramp-up challenges.

Space access, control, and surveillance are also of the greatest concern today. Only last week, Russia vetoed a UN resolution that called on countries to prevent an arms race in outer space. It’s no exaggeration to say that nuclear warheads in space are a serious threat to, among other things, our communication and GPS navigation infrastructures.

Finally, something I want to ask you. Please like, comment, forward to a friend, and/or share on social media while tagging me. I’m conducting an experiment, and am curious about the potential online reach. 🙏

Stay curious and a bit skeptical!

... Nicklas

One More Thing …

A couple of years ago, I read Cixin Liu’s The Three-Body Problem book series. It was a great read, albeit a wee bit tedious from time to time. Recently, Netflix released its adaptation based on the first book in the series. A challenging task, but I think they managed to navigate the complicated physics and political turmoil quite well. Definitely worth your time.